How China, Japan, and the U.S. Support Startups -- and What It Means for Founders and Investors

Startup ecosystems are not built by capital alone. They are shaped by the way governments, markets, corporations, universities, and investors interact. China, Japan, and the U.S. all support entrepreneurship, but the logic behind each system is very different.

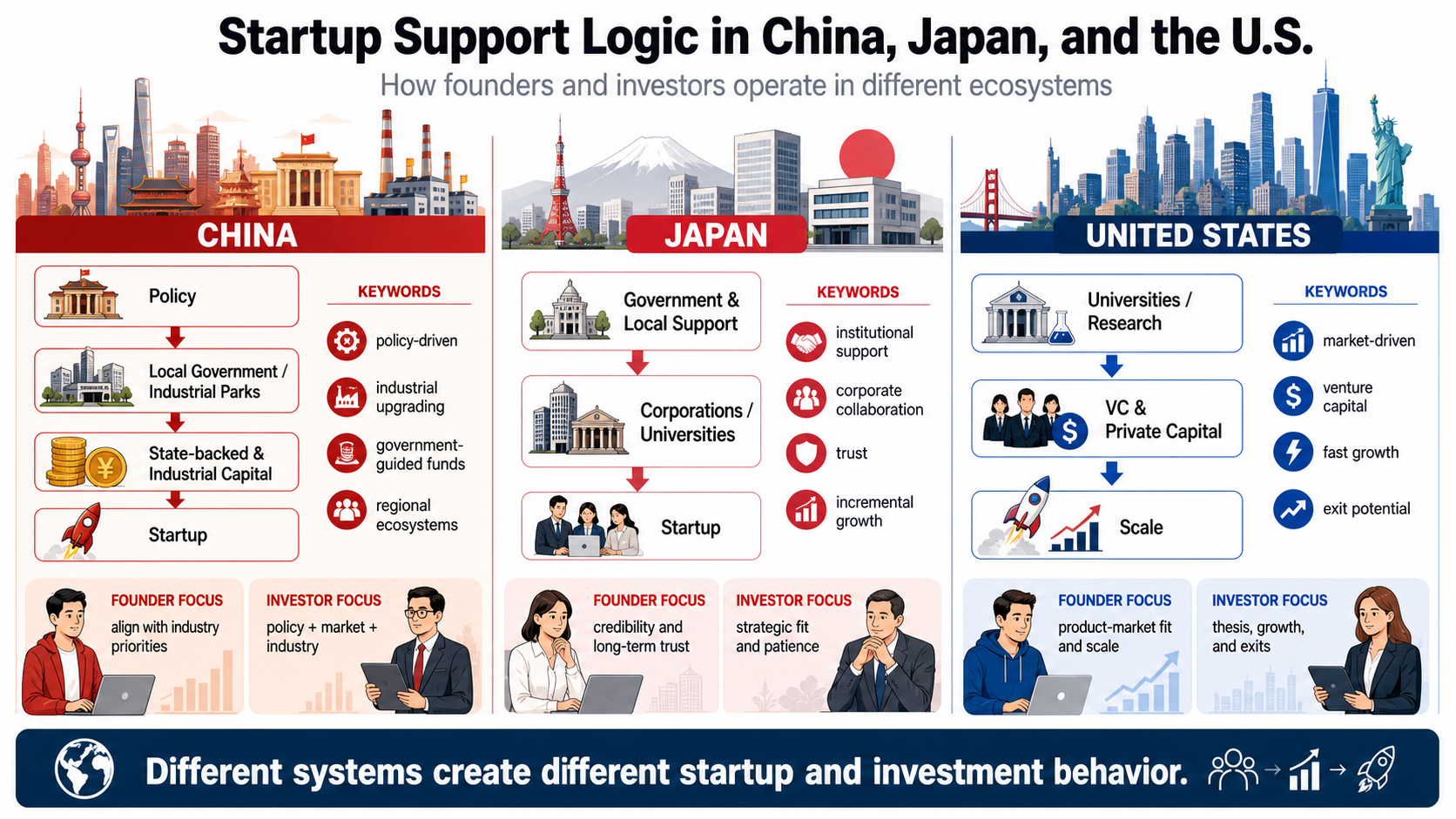

1. China: policy-driven industrial organization

China's startup ecosystem is strongly shaped by industrial policy, local governments, development zones, state-backed funds, and sector-specific priorities.

For founders, this means the key question is not only "Is there market demand?" but also:

- Does this align with national or local industrial priorities?

- Can it create employment, tax revenue, or industrial upgrading?

- Is there a suitable city, park, or local government partner?

- Can the project attract state-backed funds, industrial capital, or government-guided capital?

This system can be powerful for hard tech, advanced manufacturing, semiconductors, AI, new energy, new materials, biotech, robotics, and green technologies. Government support may provide land, subsidies, demonstration projects, policy access, and patient capital.

But the risk is that founders may become too dependent on policy signals, subsidies, or local-government incentives. A startup still needs real customers, strong execution, and commercial discipline.

For investors, China requires a dual lens: market potential and policy alignment. A good investor must understand not only technology and business models, but also regional industrial strategy, government-guided funds, state-owned capital, supply-chain localization, and exit channels.

In China, investors often operate at the intersection of policy, industry, and capital.

2. Japan: institutional support and corporate collaboration

Japan's startup support system is more institutional, structured, and incremental. National and local governments support entrepreneurship through subsidies, startup cities, JETRO, SME support organizations, university programs, and public-private initiatives.

For founders, Japan rewards credibility, reliability, technical quality, and long-term trust. The ecosystem is especially relevant for B2B startups, deep tech, university spinouts, corporate innovation, and technologies that need large-company collaboration.

The challenge is speed. Decision-making can be slow. Corporate partnerships may take time. Risk appetite is often lower than in the U.S. or China. Founders must learn how to communicate with large corporations, public institutions, and conservative stakeholders.

For investors, Japan is less about chasing hypergrowth at all costs and more about identifying technologies that can scale through industrial partnerships, global markets, and patient company building. CVCs and large corporations play an important role, especially in sectors such as materials, robotics, healthcare, climate tech, and advanced manufacturing.

In Japan, investors need patience, trust-building ability, and deep understanding of corporate strategic needs.

3. The U.S.: market-led venture scaling

The U.S. ecosystem is the most market-driven and venture-capital- oriented. Government support exists through mechanisms such as research grants, SBIR/STTR, university funding, defense-related programs, and small-business support. But the dominant logic is still private capital, large markets, fast growth, and exit potential.

For founders, the core question is:

- Is this a venture-scale opportunity?

- Can it become a large company?

- Can it attract talent and capital quickly?

- Is there a clear path to product-market fit, growth, and exit?

This system works extremely well for software, AI, biotech, frontier technologies, university spinouts, and companies with global market potential. It rewards ambition, speed, storytelling, and scalable business models.

But it can be unforgiving. Not every good business is venture- backable. Service businesses, regional businesses, and slower-growth companies may need to rely more on revenue, loans, grants, or alternative financing.

For investors, the U.S. system rewards thesis clarity, network access, founder selection, portfolio construction, and exit discipline. Venture capital is not just money; it is a mechanism for scaling companies that can become very large.

4. Different systems create different founder behavior

In China, founders often ask:

"How do I align with industrial policy and secure local resources?"

In Japan, founders often ask:

"How do I build trust with institutions, corporations, and long-term partners?"

In the U.S., founders often ask:

"How do I grow fast enough to justify venture capital?"

None of these logics is inherently superior. They simply produce different types of companies and different founder behavior.

5. Different systems also create different investor behavior

In China, investors must understand policy, local ecosystems, industrial capital, and strategic sectors.

In Japan, investors must understand corporate collaboration, technical credibility, and long-term commercialization.

In the U.S., investors must understand venture-scale markets, founder ambition, rapid growth, and exit dynamics.

A founder who succeeds in one system may struggle in another if they misunderstand the operating logic. Likewise, an investor cannot simply copy-paste one country's investment framework into another.

6. The key takeaway

Startup ecosystems are not universal. They are institutional systems.

China is policy-and-industry-driven.

Japan is institution-and-corporate-collaboration-driven.

The U.S. is market-and-venture-capital-driven.

For founders and investors operating across borders, the most important skill is not only understanding technology or capital. It is understanding the system in which technology and capital are expected to operate.

The same startup idea may need three completely different strategies in Beijing, Tokyo, and Silicon Valley.